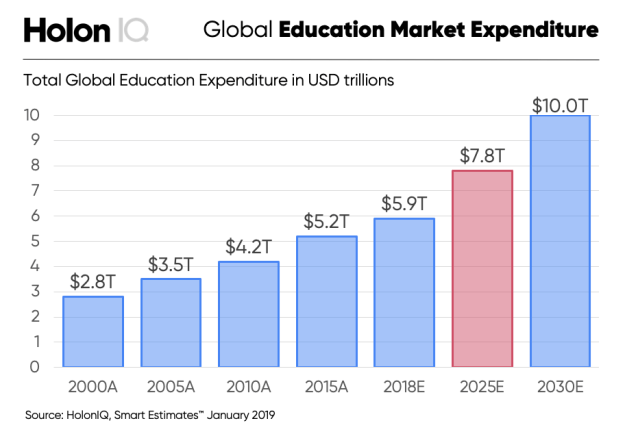

Source: HolonIQ

The promise of education markets is well marketed. Estimates have been made that global education and training spend will reach approximately $10T (that’s $10,000,000,000,000) by 2030, about 6% of global GDP, with approximately 55% spent on the K-12 sector (somewhat above $3T this year).

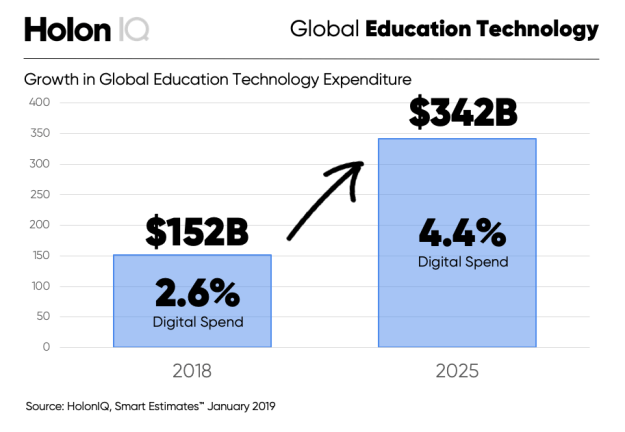

Global edtech spend is forecasted to grow from $152B in 2018 (a paltry 2.6% of total spending) to $342B in 2025 (a slightly less meagre 4.4%).

Source: HolonIQ.com

Applying technology to learning and teaching should be a massive opportunity to both improve learning impact and to build a successful business, right?

I’m convinced on both counts. But if global spend on K-12 is $3T then why is the spend on edtech so relatively modest? It’s mainly important to remember that about 80% of spending in K-12 is on teachers and other staff, with additional spending on other fixed costs such as buildings. Conceptually, in a pure-play digital future, in which teachers might be replaced with AI and robots, this could be an addressable market. However, this seems unlikely to happen at scale any time soon, since it would be not only pedagogically unsound but also socially unacceptable. (It’s my own belief that the human teacher is the “killer app” in education).

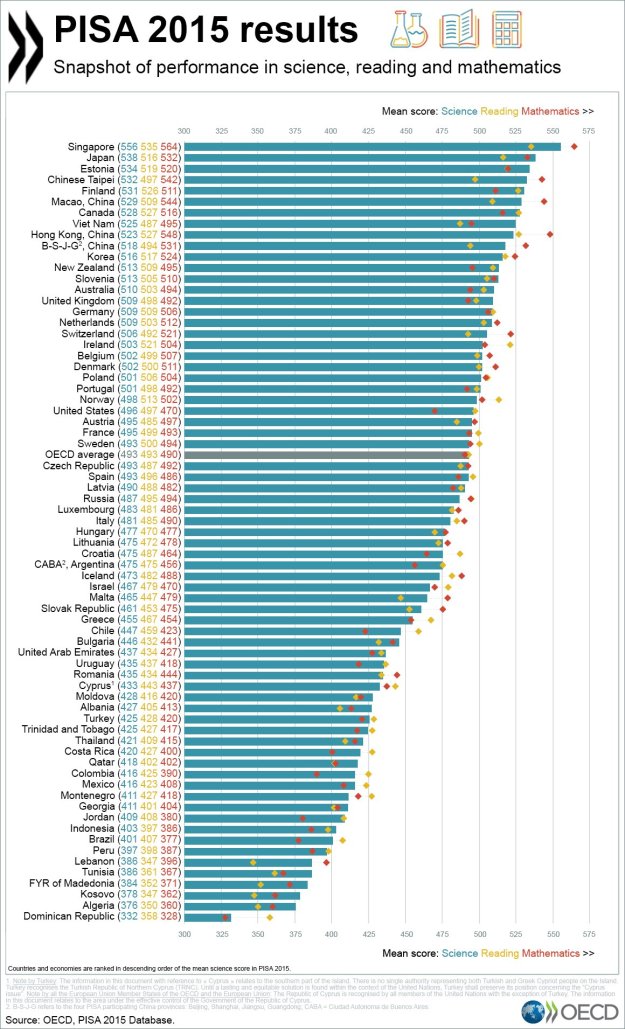

Source: OECD Education at a Glance 2018

It seems more likely that technology will be used to super-charge teachers and enable more flexible organization forms for teaching.

Is there a global market for K-12 edtech?

If we would assume for the sake of argument that 2.6% of spending on K-12 education is digital (see above), this would imply a current spend of about $85B.

I would like to understand how much success the edtech industry is having in scaling internationally. How much of the $85B is being spent on local vs global solutions and how big is the opportunity for global vendors? It’s important for us to understand this dynamic as an industry: it will inform our investment decisions and potential to make an impact on learning.

Although the edtech market is not yet very mature, it is of a sufficient scale that we should expect to see successful global operators in edtech in K-12, if the market has a (partially) global nature. Imagine we set a very low threshold: 0.025% of $85B spend, roughly $20M. How many edtech companies are there in K-12 today who are generating $20M sales or more each year on edtech offerings being sold outside their market of origin? More than 100? Less than 10? I simply don’t know, my guess is there are tens rather than hundreds or thousands.

Who is exporting more than $20M?

I am very keen to discover and understand examples of such companies (exporting more than $20M of edtech each year outside of their home markets in K-12). I would appreciate it if you would reach out to me when you know of good examples, or if you know of any good reports on the subject. (Of course there are a number of examples I am aware of and I am excluding the likes of Apple, Microsoft, Samsung and so on, which are more generic tech solutions than specifically edtech).

Assuming it’s likely the international opportunity is currently under-developed, are there things that we can do together as an industry to unlock this potential? At Sanoma we have successfully scaled our bingel platform in primary education across geographies, and are now working on the same with Kampus in secondary education. Therefore within a Group it seems to be possible. Are there other examples across Groups or through partnerships that have scaled successfully across international markets? What can we learn from these examples?

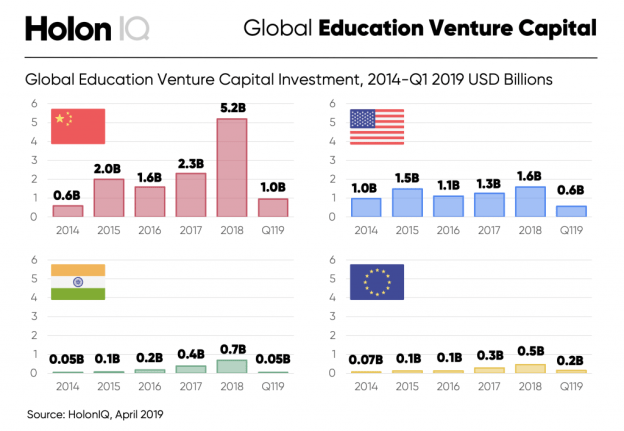

Source: HolonIQ

The Chinese, Americans and Indians have the advantage of huge internal markets. At the same time, many of their edtech ventures are focused on capturing that big local opportunity. However, it seems only to be a matter of time before some of these companies go global. Whilst lacking their scale, could we Europeans (better) develop the capability to scale across geographies as a competitive advantage in edtech? What would we need to do to make that happen?

Of course it’s a possibility that K-12 education and edtech markets will remain mainly local. In which case we as an industry can adjust some of our investment hypotheses accordingly. Yet I expect growing teacher shortages, pedagogical innovations and technological progress will drive change in our markets. We should organize ourselves to be ready for these changes.