Last week, Brighteye Ventures, a leading European investor in education technology, published the fifth edition of its European Edtech Funding Report. It looks like 2023 might be the trough of the cycle that peaked with the pandemic in 2021, and there are increasingly strong signals of a resurgence in investor appetite in 2024.

Reasons to be Cheerful

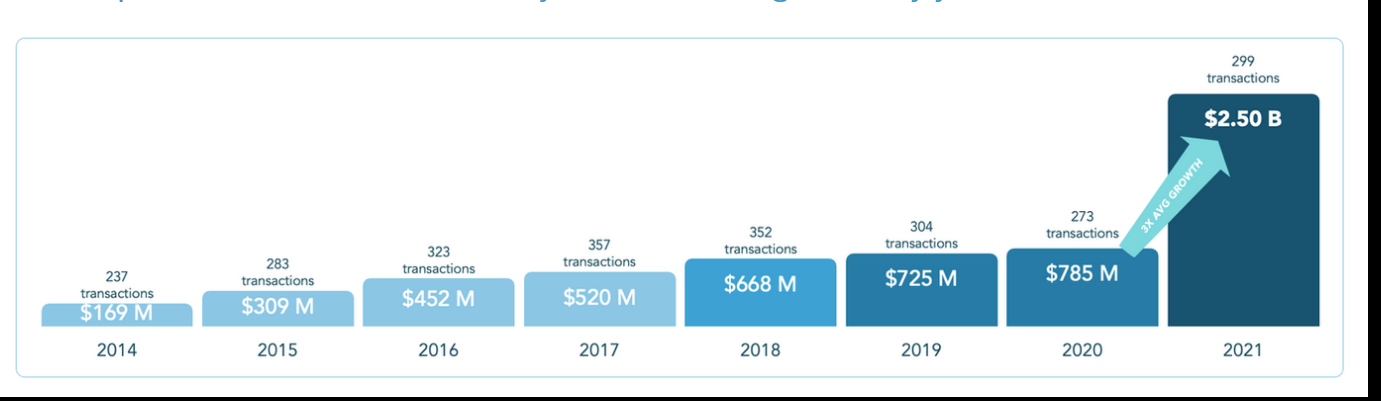

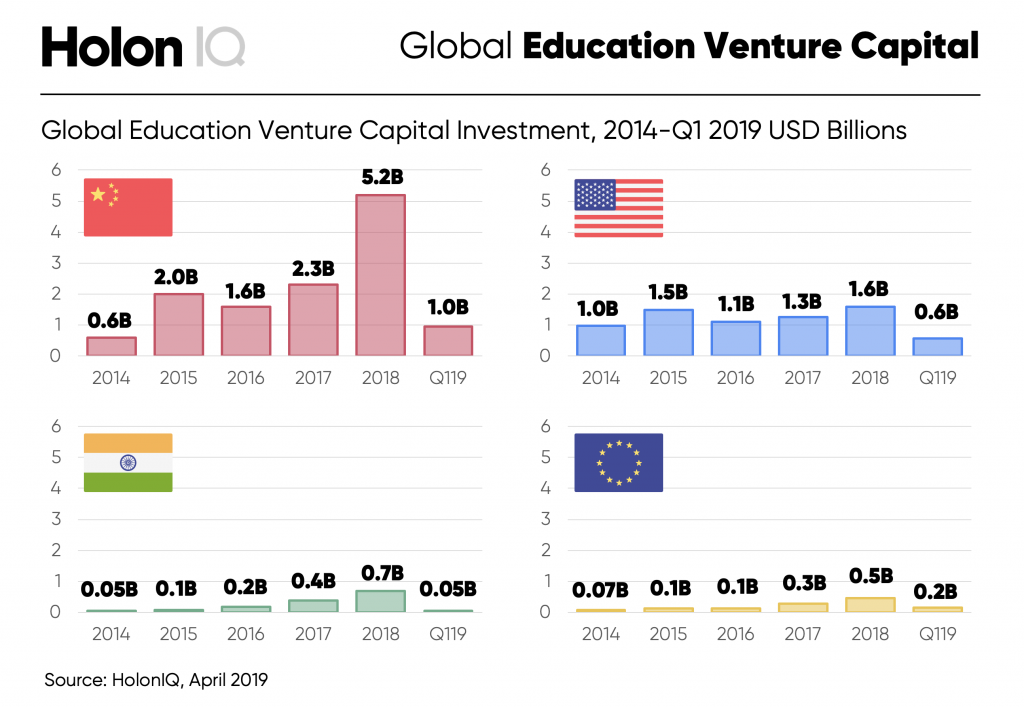

- After a period of decline, overall new venture funding for European edtech in 2023 surpassed the levels reached in 2020 ($1.2B vs $951M) and the number of deals increased on 2022 (288 vs 256).

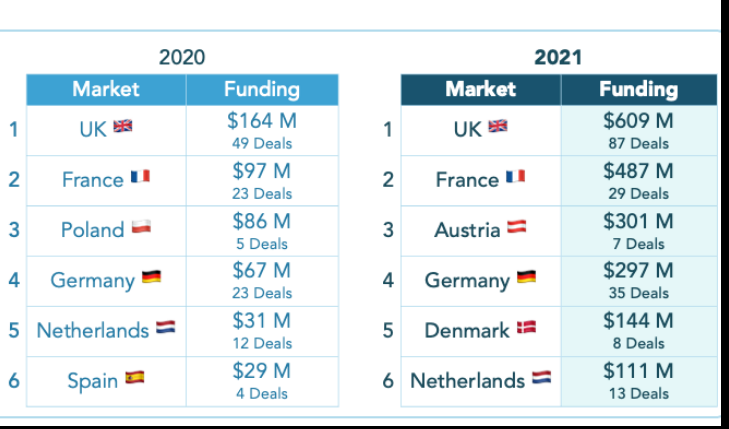

- About 1/3 of all global edtech deals took place in Europe in 2023 (a record high proportion, up from 21% in 2019), indicating a high level of investor interest in the European market.

- International private equity and venture capital investors are currently holding a record amount of dry power, with $2586B ready for deployment at the top 25 PE investors globally.

Resilience?

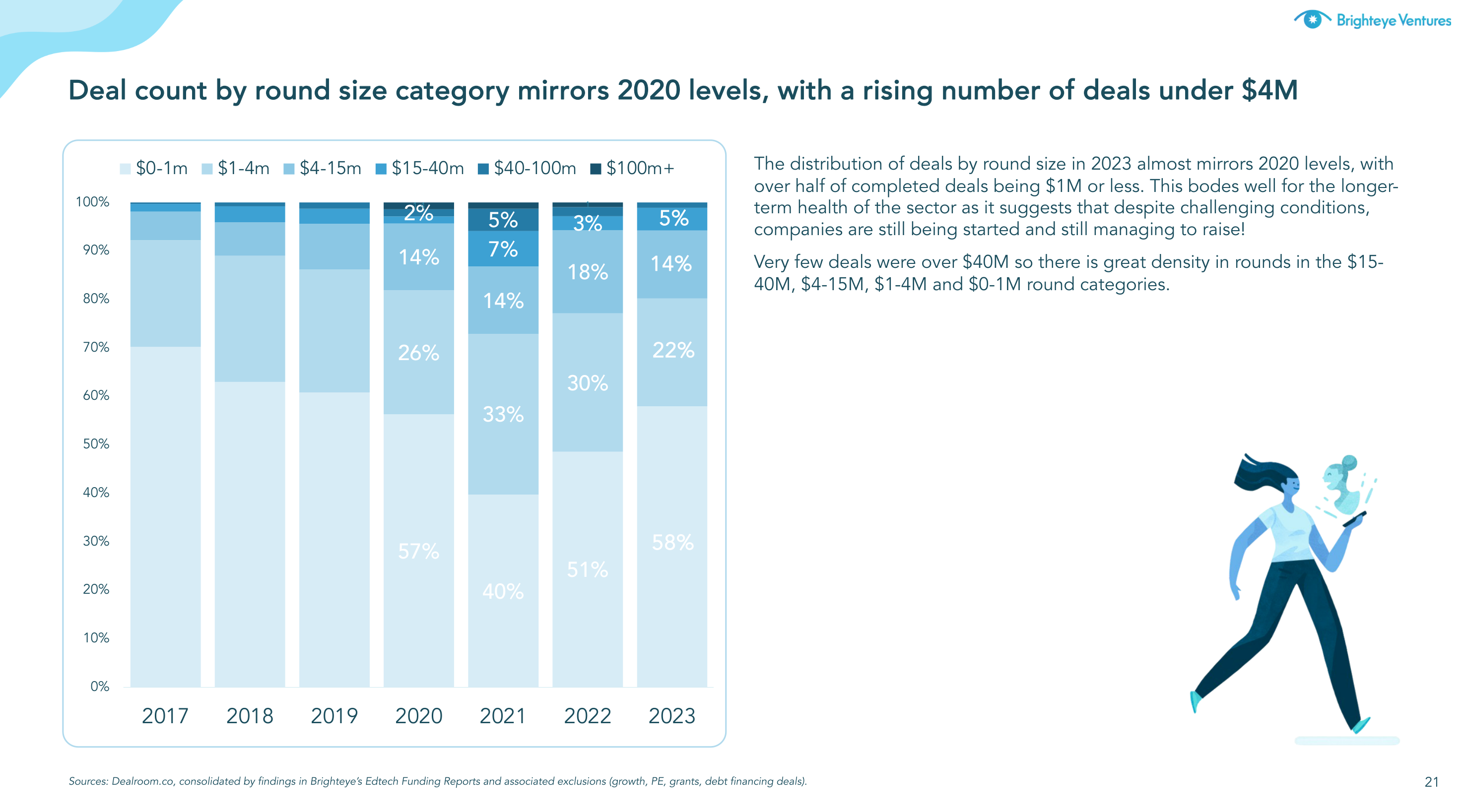

From a European perspective, “resilience in the volume of deals” was driven by a rising number of deals under $4M, with over half of the completed deals being done at $1M or less.

On the micro level of individual businesses, this thinly spread funding might make some sense, yet on the macro level of the industry and the customer, it also highlights part of the European challenge, namely lack of scale. You have to wonder if something substantial and world-class will be built out of some of these tiny deals. Usually “recessions” (possibly a relative term in tech) are a good opportunity for industries to restructure, with strong firms building on their strengths and weaker firms going out of business in what is typically a healthy evolutionary process.

Enable and simplify the work of the teacher

According to some estimates there are currently about 27,500 edtech companies in the K-12 sector, obviously not all deployed in all schools, but it’s not uncommon for schools to use hundreds of digital products. Imagine the life of a teacher. Her first concern is leading a classroom of 25-30 children, which is no mean feat in itself. When she deploys a digital solution it needs to:

a) positively impact learner outcomes

b) be easy to use and

c) ideally save time that she can use for interacting with students.

A teacher is best served by a smaller number of well-performing and frequently-used solutions than a huge toolbox of occasionally-used options.

Build a European Champion

In my view, investors in European edtech should focus on increasing scale and building a handful of segment-specific European/International Champions. At scale, a European Champion has the resources in terms of talent, know-how and money to develop and deploy top-notch learning solutions, yielding excellent learning impact and delivering good financial returns. It’s my hope (and expectation) that a group of investors will take the opportunity at this early stage in the new economic cycle to take our industry and the services we provide to schools to the next level.